Agent-based models in financial market studies

슈퍼관리자

2021-05-21

Agent-based models in financial market studies

-

Authors :

L Wang, K Ahn, C Kim and C Ha

-

Journal :

Journal of Physics

-

Vol :

1039

-

Page :

012022

-

Year :

2018

Abstract

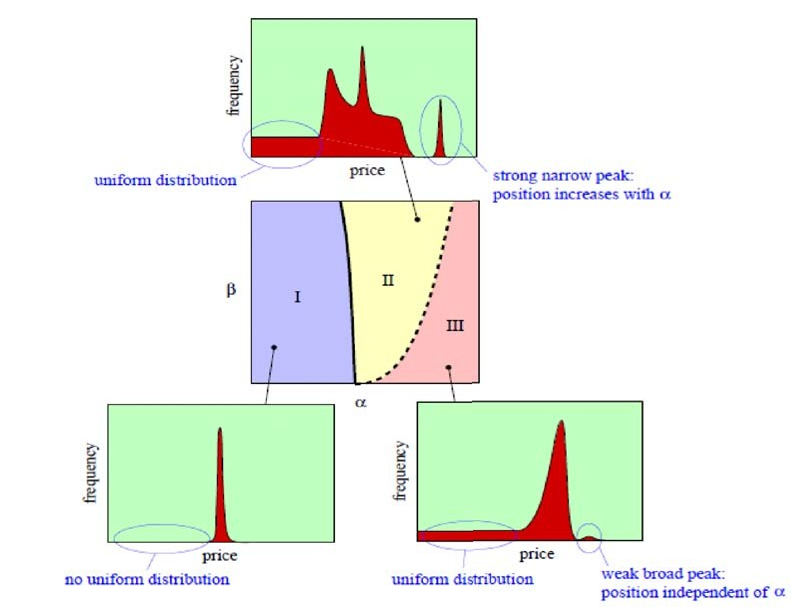

In this manuscript, we summarize prior research on the agent-based modeling of financial markets. While extensive research related to agent-based modeling has been done in various economic disciplines, we focus mainly on the evolution of the models and their applications to financial markets. A large number of studies have adopted agent-based modeling methodologies to explain various empirical findings in financial markets. Our summary shows the benefits of using such modeling to account for various financial market phenomena. We confirm that small changes in initial parameter values can lead to relatively large fluctuations through the financial markets that can be viewed as complex or chaotic systems. This also means that financial markets become volatile due to small unexpected changes in the parameters of the models that describe the market.