Measuring Financial Fragility in China

슈퍼관리자

2021-05-21

Measuring Financial Fragility in China

-

Authors :

Ahn, Kwangwon and Dai, Jacqueline and Kim, Chansoo and Tsomocos, Dimitrios P.

-

Journal :

SSRN

-

Vol :

-

Page :

-

Year :

2015

Abstract

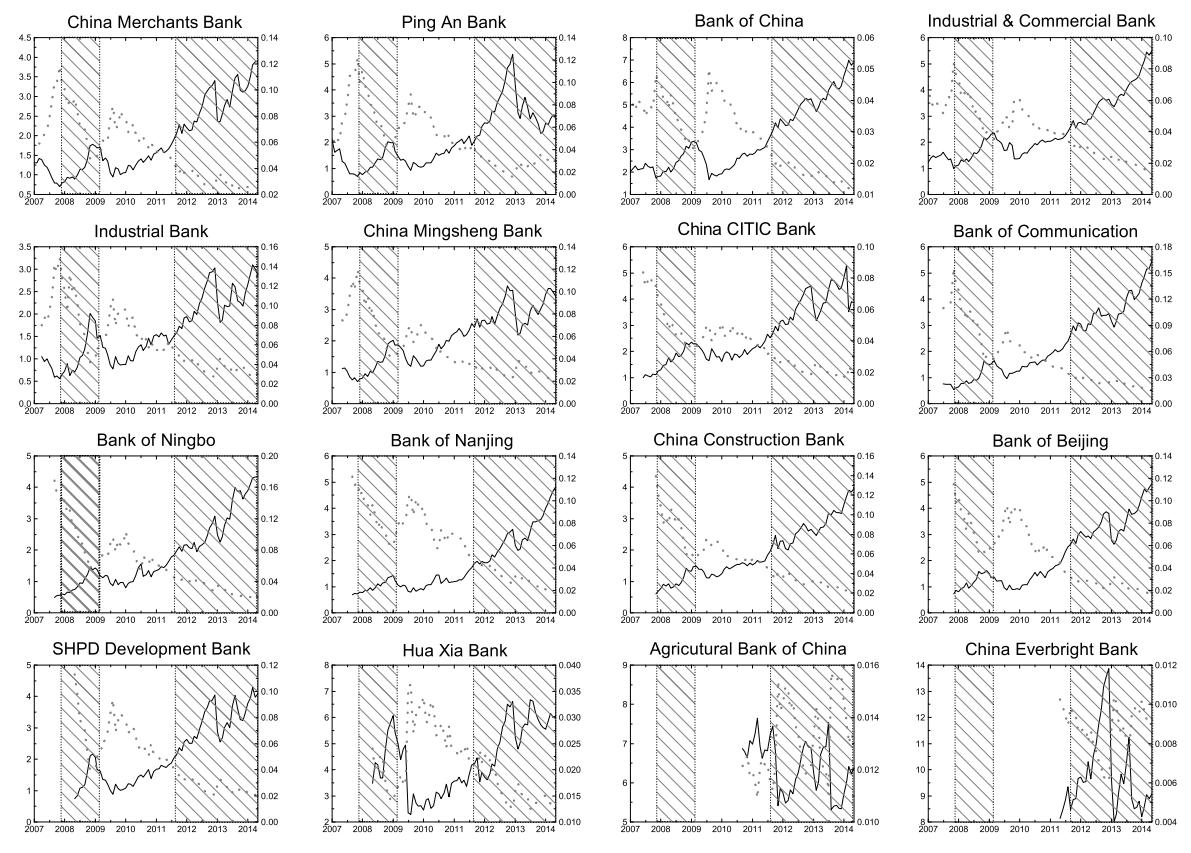

AbstractThis paper proposes a metric for a financial fragility index for the Chinese banking sector. This metric is a weighted average of two variables: bank profitability and multiple probability of undercapitalization. The weights of the two variables are assigned based on their effects on real output, estimated by a vector autoregressive model. The main contribution is two-fold: incorporating a capital adequacy ratio into a quantitative measure and aggregating insolvency risk through a multiple probability measure. We confirm that our metric successfully identifies three periods of financial turmoil accompanied by economic downturns and rules out one minor perturbation caused by side effect of the policy between 2007 and 2014. In particular, this study provides an economic rationale for the relationship among financial instability, policy, and economic activity.